{kind=link}

AdTech social has not lit up like this since Oracle acquired Moat in 2017. Back then the argument was whether independent measurement could survive inside a database company. This time the question is whether identity infrastructure can survive inside a holding company.

On Sunday, Publicis Groupe announced it is acquiring LiveRamp for $2.167 billion in an all-cash transaction, based on an acquisition price of $38.50 per share, a 29.8% premium to LiveRamp’s closing share price on May 15. The deal is expected to close before year-end 2026, with Scott Howe staying on as CEO and reporting directly to Arthur Sadoun.

The official framing from Publicis is “data co-creation to build smarter agents.” That phrase deserves to be taken seriously before it gets taken apart.

The argument is straightforward. Enterprise AI agents need differentiated data to produce differentiated outputs. No single company has enough of the right data to build that foundation alone. LiveRamp becomes the connectivity layer that makes data collaboration possible at scale. Epsilon supplies identity. LiveRamp supplies the connections. Publicis Sapient builds the infrastructure. Marcel operationalizes it across the agency.

The harder question is what changes once the open internet’s identity pipes sit inside a company with its own commercial interests.

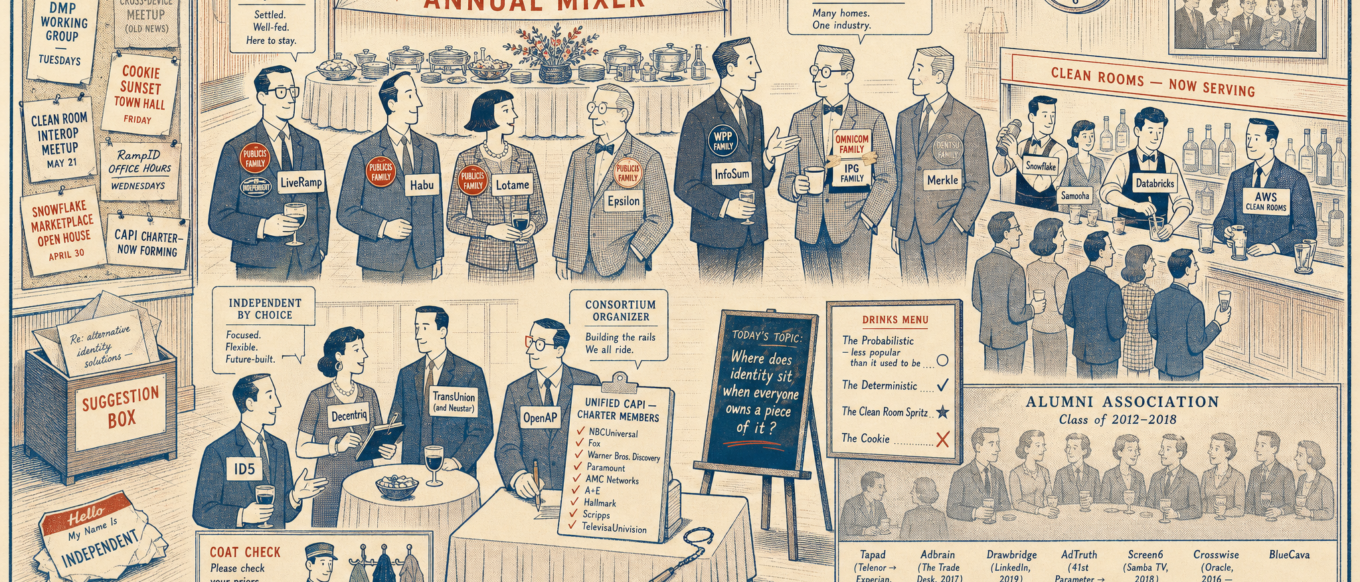

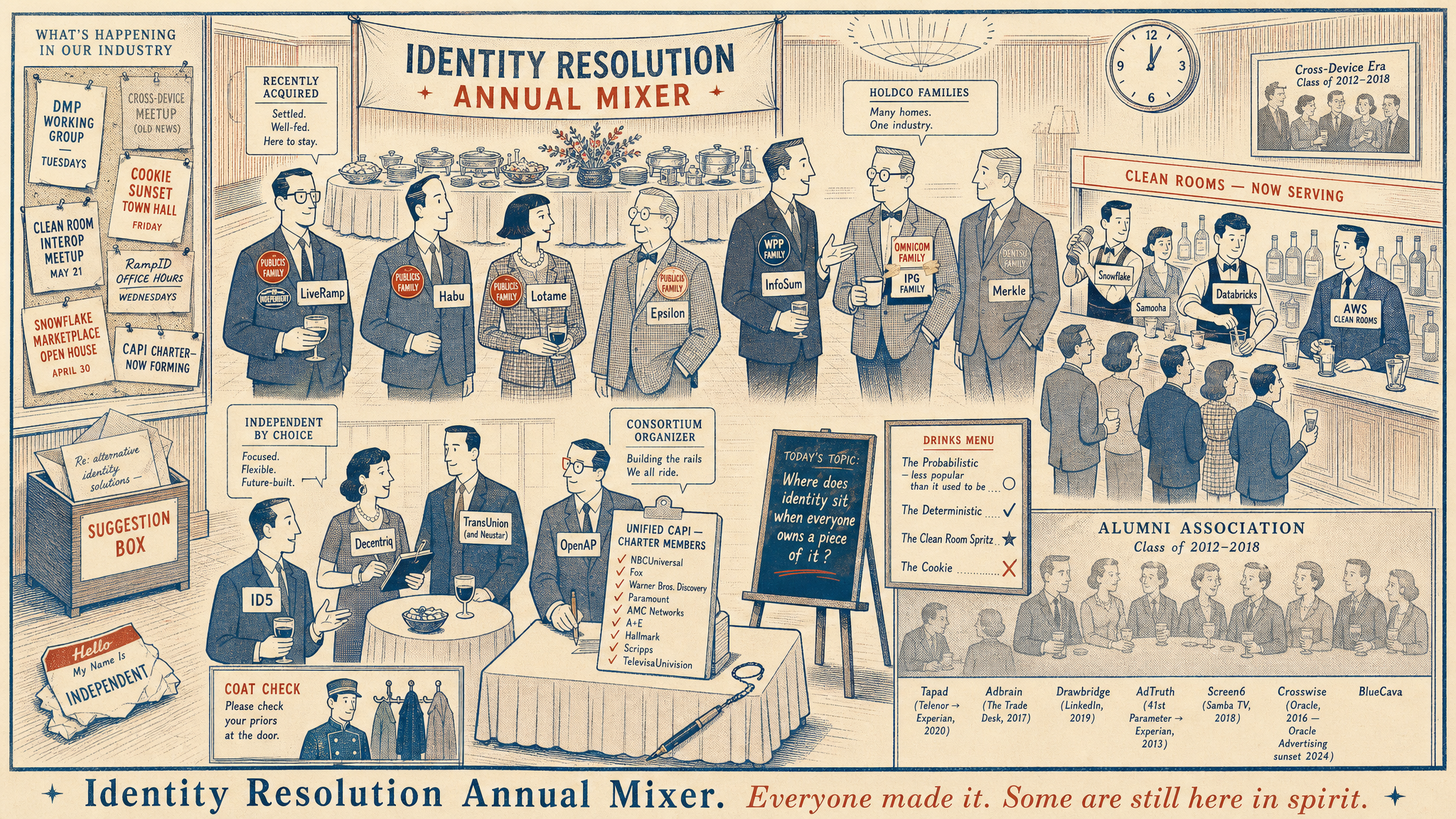

What Publicis Actually Bought

LiveRamp is not a media company. It is plumbing.

The platform sits between brand-side first-party data and the activation ecosystem. It connects thousands of publisher domains, technology platforms, and data partners across global markets.

The stack explains why the asset matters. RampID sits underneath the graph. ATS carries it through the bidstream. LocalEncoder turns messy CRM data into normalized RampIDs that can move through the ecosystem. The Marketplace layered third-party data on top, while Habu pushed the architecture further upstream into clean-room collaboration across retailers, platforms, and walled gardens.

Taken together, LiveRamp became the routing layer a huge portion of enterprise activation workflows were already built around.

That is what makes the asset strategically important. Publicis is not just acquiring an identity graph. It is acquiring the integration network that lets everyone else’s data move through the ecosystem.

Len Ostroff made the point cleanly in the post-deal commentary: LiveRamp’s moat is its integrations, not the underlying data. PII and household data are available from many sources. Keeping that data secure, normalized, permissioned, and transportable across thousands of partners is the harder thing to replicate.

The Habu acquisition also looks more strategic now than it did at the time. If AI and privacy regulation tighten how holding companies can combine customer data, the clean-room layer becomes the infrastructure that keeps the agentic story operational across markets.

The Publicis Playbook

Publicis bought Epsilon in 2019 for $4.4 billion to bring proprietary identity and first-party data assets in-house. It bought Lotame in 2025 to extend Epsilon’s identity graph with broader third-party reach. It is now buying LiveRamp to own the connectivity that lets that identity graph reach into everyone else’s media.

Publicis has been explicit that the strategy is about moving from identity resolution into AI-driven enterprise infrastructure.

- Epsilon = proprietary identity and data assets

- LiveRamp = interoperability and connectivity

- Sapient + Marcel = agentic infrastructure and workflow

- Agency services = monetization and execution

Publicis is not trying to become a DSP in the traditional sense. It is assembling the layers that determine how targeting intelligence reaches whichever execution surface the client already uses.

The company does not need to own every bidder if it can own the data foundation, the decisioning inputs, and the pipes that determine what gets passed into the bidder.

The Holding Company Pattern

WPP made a parallel move when it acquired InfoSum and integrated it into WPP Media as part of its Open Intelligence strategy.

Holding companies are no longer just buying media leverage. They are buying the infrastructure layer that determines how enterprise data flows across the ecosystem.

The advertiser pitch sounds attractive: bring your first-party data, plug into our infrastructure, and get better outcomes through proprietary co-created datasets and AI agents trained on signals you cannot access anywhere else.

The tradeoff is that the infrastructure enabling those outcomes increasingly sits inside the holding company itself.

The “Steal” Debate

Auren Hoffman, who co-founded LiveRamp and ran it through the Acxiom acquisition in 2014, called the transaction “a steal for Publicis.”

The valuation supports the argument. Publicis paid infrastructure-asset multiples for something much more strategically embedded than a typical software platform.

Auren’s broader point is that LiveRamp spent the last decade trading long-term positioning for short-term gain.

The diagnostic he points to is connections per customer. In his view, that number is surprisingly low because the platform became too expensive, too slow, too bureaucratic, or some combination of the three. The core product, defined as the onboarding and connectivity layer that gets audience data from brand-side environments to activation surfaces, has not meaningfully evolved in roughly a decade.

The infrastructure is still deeply embedded across the ecosystem, and the customer base is still enormous. The frustration comes from the feeling that the product underneath all of that stayed largely frozen while the market dynamics around it continued to change.

A new owner with conviction and capital can plausibly reinvigorate the connectivity that already exists. The incentive structure is different now. LiveRamp no longer has to optimize for the ecosystem broadly. It can optimize for Publicis clients, who collectively represent roughly $50 billion in annual media spend.

Whether an agency holding company is the right owner to do that is a different question.

The Trade Desk Conversation

The Trade Desk’s take rate has historically been justified by bundling inventory access, data targeting, and decisioning intelligence into one platform. With LiveRamp inside Publicis, alongside Epsilon and Lotame, Publicis now walks into every DSP negotiation with substantially more leverage than it had before.

Two months ago, Publicis halted spend recommendations on The Trade Desk over what was framed externally as a billing dispute. At the time, it looked like a pricing fight. Read against this acquisition, it looks more like a buyer pressuring a strategic dependency before renegotiating from a much stronger position.

Holding companies running through any independent DSP gain the same leverage. The majority of Publicis programmatic spend today flows through platforms like TTD, DV360, Amazon DSP, Yahoo, and Viant, not through Conversant, which Publicis already owns through Epsilon.

Publicis does not need to replace the DSPs its clients use. Owning LiveRamp simply gives it far more influence over the economics and data flowing through them.

The harder downstream point is that a meaningful portion of UID2’s deployable publisher coverage runs through LiveRamp’s ATS integration. ATS was one of the earliest UID2 operator-side identity providers. For a large slice of authenticated publisher coverage, the RampID-to-UID2 handshake is how UID2 gained meaningful distribution scale across the open internet.

Jeff Green has spent years arguing that the open internet beats walled gardens because transparency and independence win over closed ecosystems. Publicis is now building a data and intelligence walled garden on the buy side.

They do not need to own inventory to wall things off.

Own the identity layer. Own the data stack. Own the targeting decisions. Control the pipes that determine how those decisions reach the market.

The open internet starts looking a lot less open when the infrastructure consolidates underneath it.

Connectivity Is Not Fidelity

The Publicis framing leans heavily on data cleanliness as the prerequisite for agentic transformation.

A large share of enterprises do lack the data foundation required for AI. Co-created data, built through clean rooms and partner networks, can become a proprietary asset that fuels smarter agents.

But read carefully, this is not only a story about empowering clients. It is also a story about combining client data inside Publicis-controlled environments to create an asset that improves Publicis-controlled agents.

The bigger question is what “data” actually means at the point it enters the agent.

Activation through RampID has been an efficient way to reach a defined audience. It is also, by design, a pipeline that often hands a model the conclusion rather than the inputs that produced it.

The downstream agent does not get the behavioral fingerprint, the temporal pattern, or the upstream features. It gets the output of someone else’s model.

A model optimizing against a label is optimizing against a conclusion. That is structurally different from a model learning from evidence.

That distinction matters more as decisioning moves from rules-based bidding to AI-driven optimization. A rules-based bidder can act on the label. An AI system needs to understand the features that made the label predictive in the first place (more here).

LiveRamp is extremely good at portability. It moves identifiers, audiences, and permissions across a fragmented ecosystem. That is valuable. It is also not the same thing as preserving signal fidelity all the way to the point of decisioning.

Terry Kawaja framed the commercial version of this argument well. AI agents are commoditizing workflow automation across planning, buying, creative, optimization, and reporting. As workflow becomes cheaper, margin migrates into decisioning effectiveness. Whoever owns the inputs to decisioning captures the margin that used to live in managing complexity.

LiveRamp is not the workflow layer Publicis is paying $2.2 billion to commoditize. It is the inputs layer Publicis is paying $2.2 billion to control.

A connectivity-first architecture solves portability. Solving fidelity is a different problem.

The alternative architecture preserves raw signal deeper into the decisioning surface instead of collapsing it upstream into portable audience outputs.

That is the underlying tension this deal brings into the open.

Does the next era of advertising AI get built on connectivity to commoditized inputs, or on direct relationships to differentiated ones?

The agent is downstream of that choice.

Why Conflict Creates Opportunity

Publicis has said the right things about neutrality. The press release says LiveRamp will continue to operate as a neutral, interoperable platform with open access across the ecosystem.

A non-Publicis advertiser sending audience files through LiveRamp pipes is going to ask the same question publishers asked in 2007 when DoubleClick changed hands: are my signals informing a competitor’s commercial decisions?

The structural answer is that ownership changes perceptions around intent, priority, and roadmap, even when the contract itself does not.

Terry Kawaja called this the most significant structural shift in advertising infrastructure since that acquisition. The comparison deserves the weight he gave it. DoubleClick rewired the programmatic stack for the next eighteen years. The difference this time is where the leverage sits. Google owned inventory and acquired the ad server. Publicis owns buyer relationships and is acquiring the connectivity layer.

What happens when infrastructure the industry depends on ends up inside a company with its own commercial interest in what flows through it?

Restricting RampID delivery to non-Publicis clients would not be in Publicis’s interest. The value of the connectivity layer is correlated with the volume and diversity of partners and demand passing through it. Publicis has every reason to maintain openness where openness preserves scale.

LiveRamp’s position was always defensible on inertia. It became the default infrastructure layer because everyone else was already integrated into it.

The platform was simultaneously one of the most useful pieces of infrastructure in the ecosystem and one of the most quietly resented. For years, industry chatter framed it as a tax on connectivity the market paid because there was no practical alternative.

There was no triggering event. No reason urgent enough to move budgets, retool integrations, and abandon a working pipe.

A holding company acquisition is a triggering event.

Scott Menzer raised the sharpest version of the objection: if advertisers are happy with LiveRamp, they may simply require their non-Publicis agencies to keep using it, regardless of who owns the underlying entity. Contract-level inertia, especially among large enterprises with multi-year MSAs that name LiveRamp explicitly, will keep a meaningful portion of activation routed through LiveRamp pipes through 2027 and beyond.

The clients most likely to ask the question are the ones with active first-party data programs, media plans running through multiple agencies, and direct competitors sitting inside Publicis. Those are also the clients where the data and identity infrastructure decision carries the most strategic weight.

Independent platforms do not need to convince the entire market to rip out LiveRamp. They need to give the highest-value subset of the market a credible reason to ask whether the default pipe is still the right pipe.

The Infrastructure Split Was Already Underway

OpenAP made that point five days before the deal landed, announcing a cross-publisher Unified CAPI for TV in partnership with major TV publishers.

David Levy framed it directly: premium video needs its own intelligent operating layer to compete with walled gardens, anchored by a standardized integration point that connects advertiser conversion data with publisher exposure data.

That is a different architecture than routing every data collaboration workflow through a holding-company-owned connectivity layer.

Out-of-the-box neutral collaboration on Snowflake, Databricks, AWS Clean Rooms, and similar platforms has compressed the operational gap that Habu originally filled. Advertisers increasingly have the option to collaborate inside agnostic data platforms rather than route data through an agency-owned environment to do work they could do directly.

The displacement story is about enterprise advertisers deciding where their data should live, who should govern it, and how close it should get to the decisioning surface.

The pitch for independent identity and activation platforms does not have to be that the alternative is universally better.

It has to be that the alternative is structurally cleaner, closer to the activation surface, or built on differentiated signals the client cannot get through a generic connectivity layer.

That is a pitch the market has been waiting for an excuse to take seriously.

The Pressure Points

Will non-Publicis holding companies stay on LiveRamp pipes through the 2027 renewal cycle, or will WPP, Omnicom/IPG, Havas, and Dentsu route more audience activation through alternatives that do not carry Publicis exposure?

Will publishers continue investing in ATS integrations at the same pace, or will they accelerate parallel investments in publisher-direct identity solutions and alternative envelopes?

If Publicis routes enough of its $50 billion in client media spend toward publishers with deep ATS integration, deterministic-ID adoption among publishers could steepen. If publishers see that same integration as deepening a holding company’s identity moat, they may hedge faster.

The broader structural question is whether this deal, combined with WPP-InfoSum, accelerates the bifurcation of identity infrastructure into two categories: holding-company-owned platforms on one side, and independent infrastructure on the other.

If that happens, independence becomes more valuable, not less.

The M&A signal points in the same direction. Scaled identity, clean rooms, retail media infrastructure, measurement platforms, and proprietary consumer datasets all look more strategically scarce after this deal than they did before it.

The Through Line

The official narrative is that this deal is about agents.

The market narrative is that it is about leverage.

Both are true.

What changed on Sunday was not the technology. The pipes are the pipes.

What changed is who owns them, and what ownership implies about every audience flow that touches them.

LiveRamp solved a real problem for the industry. The acquisition does not undo that. It resets the question of whether the solution should sit inside a holding company.

The market will answer that question with budget, not tweets.